PM’s ‘Apna Ghar’: Your guide to getting a Rs10m housing loan

3 min read

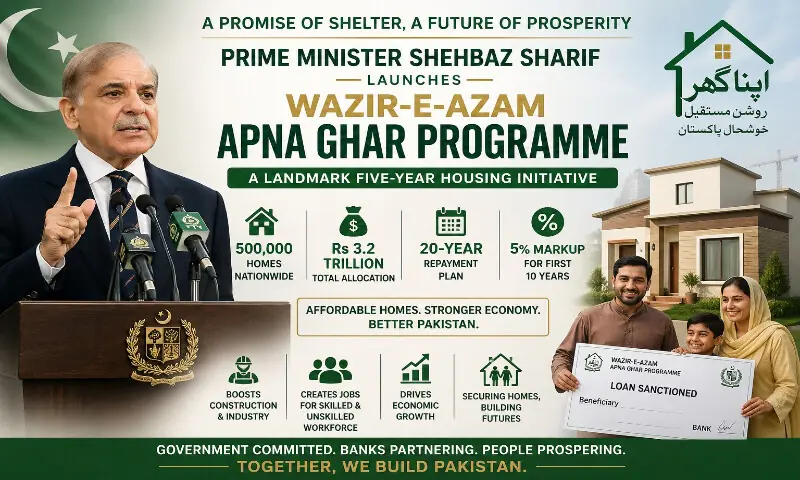

Prime Minister Shehbaz Sharif on Thursday launched the ‘Apna Ghar’ housing scheme, a major initiative aimed at helping low-income families build or buy homes through subsidised bank loans of up to Rs10 million.

Unveiled in Islamabad, the five-year programme will provide financing for 500,000 houses at an estimated cost of Rs3.2 trillion.

The government says the scheme is designed not only to address Pakistan’s housing shortage but also to boost employment and stimulate construction-related industries.

Calling housing a “basic right of every citizen,” the prime minister said the scheme will be implemented nationwide, including all four provinces, Azad Kashmir and Gilgit-Baltistan.

When does it start and what’s the target?

Applications for the scheme opened on April 29. In the first year alone, the government aims to facilitate 50,000 homes. Borrowers will be given up to 20 years to repay the loan.

How much loan can you get?

Under the scheme, applicants can secure financing of up to Rs10 million. However, buyers must arrange at least 10% of the property’s cost themselves, while banks will finance up to 90%.

The loan structure is divided into four tiers:

- Up to Rs2.5 million

- Up to Rs5 million

- Up to Rs7.5 million

- Up to Rs10 million

What can you buy or build?

The scheme offers flexibility for different housing needs:

- Purchase of a newly built house (up to 10 marla)

- Buying an apartment or flat (up to 1,500 sq ft)

- Construction on an already owned plot

- Purchase of a plot along with construction financing

Who is eligible?

To qualify, applicants must:

- Be Pakistani citizens with a valid CNIC

- Be first-time homebuyers

- Be aged between 20 and 65 years

- Have a minimum monthly income of Rs40,000

Salaried individuals must show at least six months of employment, while business owners need two years of experience. Close family members can apply jointly to increase eligibility.

Banks will assess applicants’ income and expenses to ensure they can comfortably repay monthly instalments.

Ownership and loan terms

The property will be registered in the applicant’s name. However, the bank will retain the original documents as collateral until the loan is fully repaid. Once cleared, the borrower will receive a no-objection certificate (NOC), and full ownership rights will be restored.

Interest rate and repayment

The loan tenure is up to 20 years. The markup rate is set at 5% for the first 10 years, after which it will shift to a market-based rate.

How to apply?

Applicants will soon be able to apply through an official online portal. Alternatively, they can visit branches of commercial banks, Islamic banks, or housing finance companies.

Required documents include:

- CNIC

- Proof of income (salary slip or business details)

- Property documents (if applicable)

Banks are required to process applications within one month, and no processing fee will be charged.

Economic impact

The government says the initiative will not only provide affordable housing but also create jobs, accelerate construction activity, and support broader economic growth.

PM Shehbaz also urged banks to actively support the programme, warning of strict action against those who fail to facilitate applicants, while promising recognition for institutions that perform well.

For the latest news, follow us on Twitter @Aaj_Urdu. We are also on Facebook, Instagram and YouTube.

Comments are closed on this story.